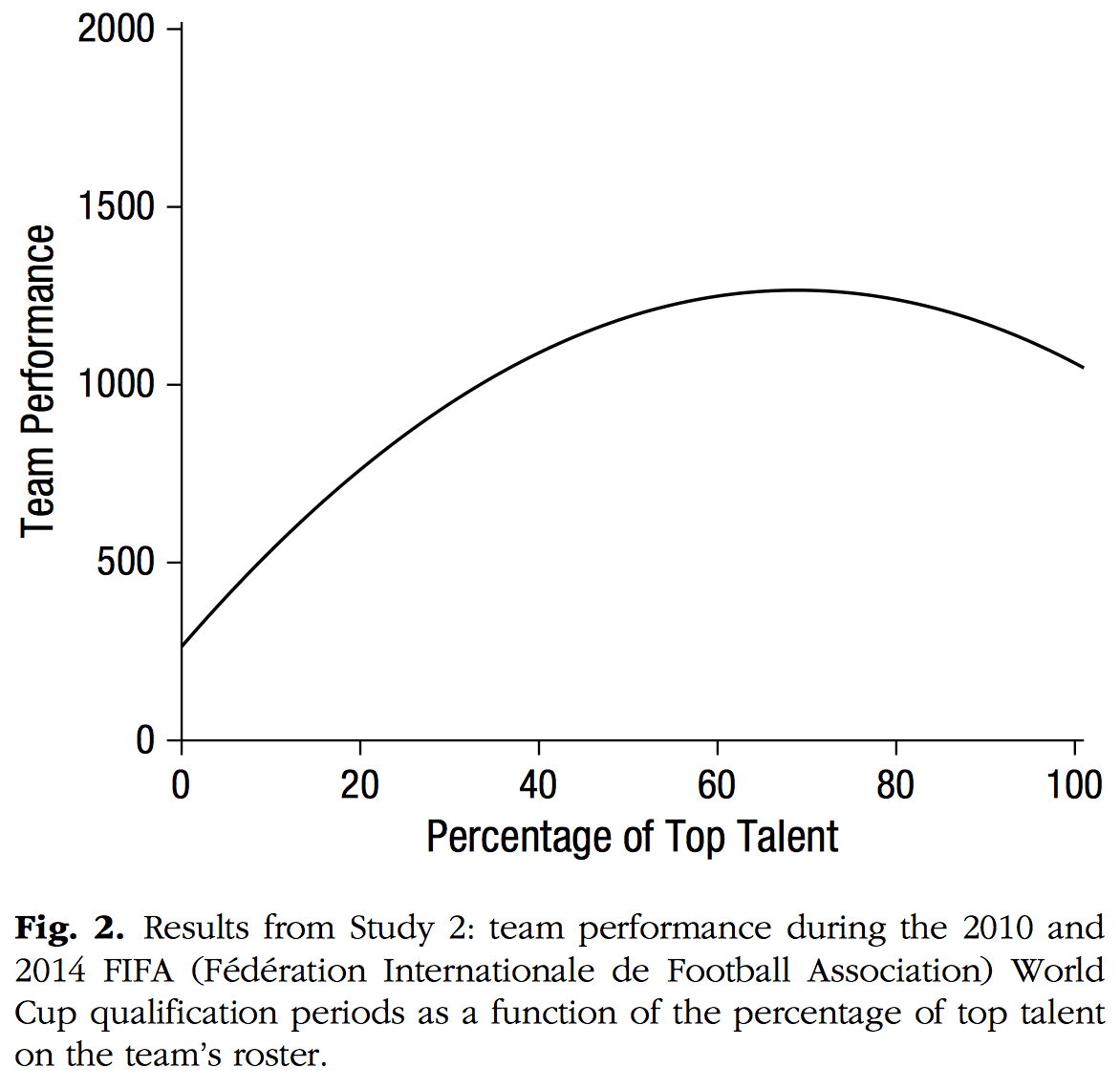

A few days ago we discussed a paper from 2005, Competition and Innovation: An Inverted-U Relationship, two of whose authors recently won the Nobel prize in economics.

I had some concerns about the analysis, which I can express with reference to the above figure from that paper:

1. The paper’s all about an inverted U relationship, but this is driven by fitting a quadratic curve rather than, say, a curve with diminishing returns.

2. The line does not seem to go through the data points. In particular, the curve seems to be too low at the rightmost part of the graph–an artifact of fitting a quadratic, perhaps?

3. The y-axis is some weighted count of patents but it’s being used as a measure of the more abstract concept of “innovation.”

4. The x-axis is an average of profit margins but it’s being used as labeled a measure of the more abstract concept of “competition.”

5. The model predicts patents from profit margin in the same year, but to the extent the model is appropriate I think you’d expect a lag.

6. They use Poisson regression, but the data are not counts, also if you don’t somehow correct for overdispersion your standard errors will be too low.

The plan

Here are the ways I’m gonna adjust for the above issues in my reanalysis:

1. I’ll fit a quadratic curve to replicate what they did in the paper, and I’ll also fit another family of curves (the “hinge”) that allows for nonlinearity but without enforcing non-monotonicity.

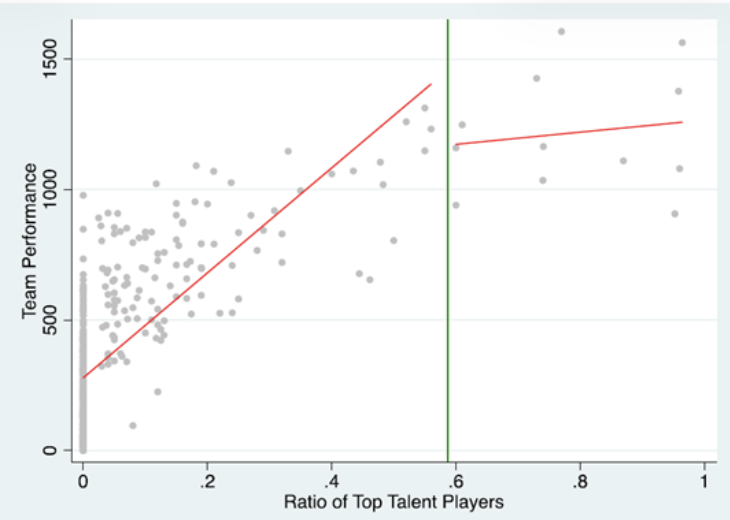

2. One problem with the above graph is that it excludes 20% of the data (see the figure caption). I’ll plot the fitted curves showing all the data. Another possible reason for the problematic fit is that in the paper they say they adjust for industry and year effects, and so I’ll make a plot showing the fitted curve and the data broken down by industry. I’ll do the adjustments in two ways: “fixed effects” as in the published paper (using various R packages), and multilevel modeling (using Stan).

3, 4. I’ll relabel the axes of the graph to more accurately capture the authors’ measures of competitiveness and innovation, but I’ll swallow the concern that the analysis only uses a subset of the data that were available at the time (from the paper, “Our sample includes all firms with names beginning “A” to “L” plus all large R&D firms. After removing firms involved in large mergers or acquisitions and those with missing data . . .”).

5. This lag thing is an issue, but I have enough concerns with items 3 and 4 that it’s hard for me to take the paper’s theoretical and causal arguments seriously. But, sure, you could replicate my analyses at different lags.

6. I’ll compare four sorts of models: Poisson, quasipoisson, negative binomial, and normal regression on log(y+1). Quasipoisson and negative binomial are two different ways to correct Poisson regression for overdispersion. Modeling on log(y+1) is a completely different way to model data that are mostly positive but have some zeroes, and I think it actually makes the most sense for this example, as the data are not actually counts. When fitting Poisson and negative binomial regressions, I’ll round the data to the nearest integer, which turns out to essentially not affect the results.

The above is not a preregistration plan; I wrote it in the middle of the project after doing some of the analyses already.

The data

Bradford in comments links to a post from 2014 by Leif Nelson and Uri Simonsohn that includes a file linking to the website of Nicholas Bloom, one of the authors of the paper. Navigating the site takes me to this page with a link to a zip file with the data, which I then downloaded.

Good job by Bloom to post the data from a paper published in 2005. I’m not so good with data availability myself.

The data file has 354 records, including data from 1973-1994 and from 17 industries, and for each of these records it has the weighted patent count (“patcw”), the measure of profit margin (“Lc”), and a bunch of variables that I didn’t try to figure out, because these are all I need to replicate the main analysis. (The file does not seem to include a code book, but I’m not complaining, as they’re already way ahead of me by making the data available at all.)

Initial data analysis: quadratic regression using Poisson, quasipoisson, and negative binomial models

I get going by plotting the data and fitting some quadratic models:

Compared to the graph at the top of this post, the above plot shows more data (I’m not trimming the upper and lower 10% of observations), and the quadratic curves are much flatter than were shown in that paper:

(1) green curve: poisson fit to rounded data (using glm() in R)

(2) red curve: quasipoisson fit to rounded data (using glm())

(3) blue curve: quasipoisson fit to raw data (using glm())

(4) pink curve: negative binomial fit to rounded data (using glm.nb())

(5) orange curve: negative binomial fit to rounded data (using stan_glm())

The first four curves are so similar that the lines overlap and you can’t see the green and red curves: They’re there, just overwritten. For each model I display the point estimate of the curve (best fit for models 1-4, posterior median for model 5). In the models above, quasipoisson uses the Poisson fit and then adjusts standard errors to account for overdispersion; negative binomial is a probability distribution that accounts for overdispersion in a different way.

We went from 1 to 2 to see if switching to quasipoisson made a difference (it did; the standard error was much bigger after we allowed for overdispersion); we went from 2 to 3 to see if rounding made a difference (it did’t for these data); we went from 3 to 4 to see if switching to negative binomial made a difference (it didn’t do much, but the standard error increased slightly); and we went from 4 to 5 to see if switching to full Bayes made a difference (it looked a lot different, actually).

I’ll put the code at the end of this post so as not to distract from the story. Here are the relevant pieces of console output:

(1) poisson fit to rounded data

coef.est coef.se

(Intercept) -74.82 25.85

Lc 164.76 54.90

I(Lc^2) -88.39 29.14

(2) quasipoisson fit to rounded data

coef.est coef.se

(Intercept) -74.82 84.64

Lc 164.76 179.78

I(Lc^2) -88.39 95.44

(3) quasipoisson fit to raw data

coef.est coef.se

(Intercept) -75.01 84.01

Lc 165.13 178.43

I(Lc^2) -88.55 94.72

(4) negative binomial fit to rounded data

Estimate Std. Error

(Intercept) -80.80 89.49

Lc 177.20 190.10

I(Lc^2) -94.85 100.92

(5) negative binomial fit to rounded data (Bayesian)

Median MAD_SD

(Intercept) -7.1 33.2

Lc 21.1 69.5

I(Lc^2) -12.2 37.3

In a paper I’d prefer to display these uncertainties graphically; here I’m giving the console output to give a sense of how things might go in our usual workflow of fitting models and looking at them. Here you can see that the quadratic terms all have large standard errors–except for the very first model, the Poisson, but its standard error is too low as it does not account for overdispersion.

The only thing that really puzzles me here is what’s going on with model 5. Could it be that the Bayesian model uses the posterior median rather than the optimum? I’ll check by re-fitting it, running stan_glm on “optimizing” setting:

(5_opt) negative binomial fit to rounded data (Bayesian posterior mode)

Median MAD_SD

(Intercept) -5.3 36.8

Lc 17.1 76.7

I(Lc^2) -10.9 39.4

That’s not much different from the posterior median. So I guess the difference between the negative binomial regressions fit by glm.nb() and stan_glm() arise from differences in the fitting algorithms, or maybe something I missed in the coding. If I wanted to proceed further down this track I would have to investigate this a bit further, reading up on what glm.nb is actually doing in R, and in Stan programming the negative binomial model myself from scratch and also comparing to brms.

For now I’ll just move on. My guess is that the difference in fits has something to do with how seriously the model takes the small number of influential data points near the top of the graph, but I’ll set that aside for now because we’ll be fitting some more models.

Quadratic regression adjusting for industry and year effects

The next step is to adjust for industry and year effects, which I’ll do in a few ways. I’ll aid in the interpretation of these by plotting the data and fitted curve separately for each industry. In the data the industry codes took on 17 different values ranging from 22 to 49, which according to the paper correspond to “two-digit SIC codes.” So I googled “two-digit SIC codes,” which are listed in various places online. I could not find an official link, but various unofficial sources seemed to agree; here’s one such list.

For each plot, black dots show the data for that industry, with a large dot showing the data from the first year of the data and thin black lines showing the time sequence. The colored curves are the fitted quadratics for each industry in an average year, as explained below.

It’s kind of weird that Furniture has so many patents, and that the number of patents for machinery and computers started out high and then dropped, and that electric and gas services had no patents for the first few years and then suddenly had a lot . . . this is just what’s in the data. I checked a few things to make sure I didn’t garble the categories but it’s possible that I’m missing something.

Here are the models I fit:

(3a) blue curve: quasipoisson fit to rounded data, including factors for industry and year (using glm())

(4a) pink curve: negative binomial fit to rounded data, including factors for industry and year (using glm.nb())

(5a) orange curve: negative binomial fit to rounded data, including factors for industry and year (using stan_glm())

(6a) purple curve: multilevel negative binomial fit to rounded data, with varying intercepts for industry and year (using stan_glmer())

Models (3a), (4a), and (5a) include unmodeled coefficients for industry and year (“fixed effects,” in economics jargon); model (6a) considers these coefficients as latent variables and estimates their distributions (this is what economists call “random effects”).

From the above graph you can see that, after adjusting for industry and year effects, the quadratic curves are much stronger. Most of this comes from the industry effects; there’s not much evidence for unexplained variation at the year level. Here’s the relevant console output from model (6a), which conveniently estimates the scale of each batch of varying intercepts:

stan_glmer

family: neg_binomial_2 [log]

formula: patcw_rounded ~ Lc + I(Lc^2) + (1 | sic2) + (1 | year)

observations: 354

------

Median MAD_SD

(Intercept) -68.3 27.1

Lc 146.6 57.5

I(Lc^2) -77.9 30.9

Auxiliary parameter(s):

Median MAD_SD

reciprocal_dispersion 5.6 1.0

Error terms:

Groups Name Std.Dev.

year (Intercept) 0.11

sic2 (Intercept) 2.11

Num. levels: year 22, sic2 17

In this fitted model (6a), and also in (4a), and (5a), not shown here, the estimated coefficient for the quadratic term is a bit more than 2 standard errors away from zero, that is, statistically significant at the conventional level. The estimated quadratic term in (3a), the quasipoisson regression, is a bit more than 4 standard errors from zero; I guess this difference is attributable to the different ways that the quasipoisson and negative binomial effectively weight the extreme values in the data.

Quadratic regressions on log(y+1)

When modeling count data we usually start with the negative binomial model with log link. And here I wanted to connect to whatever version of Poisson regression was used in that published paper.

But, as noted above, these data aren’t counts–they’re not even integers, and I think it makes sense to just directly model them on the log scale. Some of the observations have zero values, though, and so I’ll follow the standard practice of modeling nonnegative data y by fitting regressions to log(y+1). My general recommendation along these lines is to model log(y+A), where A is some constant that corresponds to a baseline level of the data. In this case, the 354 data points include 46 zeros, then another 60 values between 0 and 1, then various values (none of them are integers!) ranging as high as 44.7. For the purpose of studying patent counts as measures of innovation, it seems reasonable to add 1 to these data, which blurs the lowest values (there is no big distinction between 0 and the lowest nonzero observation, 0.037) while preserving the distinction between the higher levels. This seems about right: to the extent these data will be supplying a signal on innovation, we’ll want to mostly be learning from data on the high end.

Here’s what happens when we fit the quadratic regression, not adjusting for industry and year effects, to the log(y+1) transformed data. Now we can just use normal errors and we don’t have to worry about Poisson or negative binomials, so there’s just one curve:

You can see the zeros at the very bottom of the graph. The model of normally-distributed errors:

(7) green curve: normal regression fit to log(y+1) (using lm())

is not perfect, but I think it’s close enough, and we no longer have to worry about exactly how we’re modeling extremely high values. On the log scale we still see a fitted quadratic curve. The fit is noisy–the coefficient for the quadratic term has a standard error that is much higher than the estimate itself–but, again, let’s move on to the regressions that adjusts for industry and year effects.

As before, we show the data and fit (this time, with both on the log(y+1) scale) broken out by industry:

The curves come from two fitted models:

(8) orange curve: normal regression fit to log(y+1), including factors for industry and year (using stan_glm())

(9) purple curve: multilevel regression fit to log(y+1), with varying intercepts for industry and year (using stan_glmer())

They’re pretty similar; I assume that the small differences between the two fits arise from the fact that the least-squares model (8) does more adjustment for industries. The estimated coefficients for the quadratic terms are 3 or 4 standard errors from zero. Here’s the output from model (9):

family: gaussian [identity]

formula: log_patcw ~ Lc + I(Lc^2) + (1 | sic2) + (1 | year)

observations: 354

------

Median MAD_SD

(Intercept) -86.8 24.6

Lc 186.6 52.5

I(Lc^2) -98.6 27.9

Auxiliary parameter(s):

Median MAD_SD

sigma 0.5 0.0

Error terms:

Groups Name Std.Dev.

year (Intercept) 0.09

sic2 (Intercept) 1.04

Residual 0.47

Num. levels: year 22, sic2 17

Hinge regression on log(y+1)

As we have discussed already, the big problem with quadratic regression is that it enforces non-monotonicity. I’d like to fit a model that allows nonlinearity but without a declining slope automatically turning into a negative slope.

My first thought was to fit a model with an asymptote, something like this: b_0 + b_1*(1 – exp(x/b_3)), as an alternative. But this curve has the opposite problem: it is restricted to be monotonic. What I really want is a model that can have diminishing returns or can asymptote or can have that inverted U shape, with the question answered by the data.

We have such a model–the hinge function:

This is a curve that smoothly connects two straight lines which can have arbitrary slopes. The parameters of the curve are:

x0: the value of x where the two lines would intersect

a: the value of y where the two lines would intersect

b0: the slope of the line on the left side of the hinge

b1: the slope of the line on the right side of the hinge

delta: the scale of the continuous curve connecting the two lines

For our purposes, we are most interested in b1: is there evidence that this slope is negative?

We program the hinge model in Stan–the code’s right there at the linked post–also including a multilevel model with varying intercepts for industry and year, as above. Here’s the whole program:

functions {

vector logistic_hinge(vector x, real x0, real a, real b0, real b1, real delta) {

vector[size(x)] xdiff = x - x0;

return a + b0 * xdiff + (b1 - b0) * delta * log1p_exp(xdiff / delta);

}

}

data {

real<lower=0> delta;

int N;

vector[N] x, y;

int J1, J2;

array[N] int<lower=1,upper=J1> group1;

array[N] int<lower=1,upper=J2> group2;

}

parameters {

real x0;

real a, b0, b1;

real<lower=0> sigma, sigma1, sigma2;

vector<offset=0, multiplier=sigma1>[J1] a1;

vector<offset=0, multiplier=sigma2>[J2] a2;

}

model {

x0 ~ normal(1, 1);

a ~ normal(0, 100);

b0 ~ normal(0, 100);

b1 ~ normal(0, 100);

a1 ~ normal(0, sigma1);

a2 ~ normal(0, sigma2);

y ~ normal(logistic_hinge(x, x0, a, b0, b1, delta) + a1[group1] + a2[group2], sigma);

}

When fitting the model, we specify the scale parameter delta, setting it to 0.05, which allows for a gentle curve within the range of the data (as you can see from the plots above, x ranges from about 0.85 to 1.0). There’s some arbitrariness here, but it’s just too hard to fit this parameter directly from the data. In effect this curvature is hard-coded into the quadratic regressions fit earlier.

We assign weak priors to the other parameters in the data, effectively excluding extreme values for the slopes of the curves. The only one of these priors that might be confusing is the prior for x0, the x-position of the hinge. We’re soft-bounding it at the high and low ends just so that the fit won’t get lost in extreme values: once x0 is far outside the range of the data, the curve effectively becomes a straight line and the location of the hinge becomes non-identified.

So, yeah, the hinge is a bit more work to fit compared to the quadratic, but that’s the price we have to pay to fit a more flexible model to this small dataset. And in this case I think the flexible model is absolutely necessary given the goal of seeing whether the data indicate that inverted U shape.

Here’s the result:

In each plot, the blue curve represents the posterior median of the parameters and the red curves correspond to 20 draws from the posterior distribution.

Here’s the summary of inferences:

variable mean median sd mad q5 q95 rhat ess_bulk ess_tail

lp__ 71.69 71.85 6.65 6.87 60.81 82.19 1.00 838 1428

x0 0.94 0.93 0.07 0.09 0.82 1.05 1.04 132 1204

a 4.03 4.03 0.72 0.69 2.84 5.23 1.01 1178 1549

b0 52.71 36.93 42.67 24.45 15.29 146.35 1.03 251 1288

b1 -50.66 -31.22 46.50 22.85 -149.89 -11.44 1.03 146 883

sigma 0.47 0.47 0.02 0.02 0.44 0.50 1.00 4279 2726

sigma1 1.11 1.08 0.21 0.20 0.81 1.50 1.01 880 1217

sigma2 0.08 0.08 0.04 0.04 0.02 0.16 1.00 999 1301

a1[1] -0.25 -0.25 0.30 0.30 -0.74 0.26 1.00 486 736

a1[2] 0.23 0.22 0.30 0.30 -0.26 0.75 1.00 491 1036

...

The key parameter is b1, the slope on the right side of the curve. The posterior mean is -50.66 with standard error 46.50–so, apparently, not statistically significant–but if you look at the posterior quantiles, you’ll see that the distribution is very skewed. Indeed, it turns out that all 4000 of the posterior simulation draws of b1 are negative here.

So, after all this modeling, it seems that the data do clearly indicate an inverted U pattern!

That said, I haven’t explored the hinge model too carefully. For example, when I re-fit it with some other choices of the hinge scale parameter delta, it sometimes doesn’t mix well. I think the above graph with delta=0.5 fits these points about as well as is possible, so I’m ok with it as a data summary, but I’m not saying that my fitting procedure is fully computationally robust. If I were to be working more on the computation for this particular problem, I’d start by removing the year effects, as they can be adding stress to the computation without affecting the fit in any meaningful way.

Before getting to the interpretation of these results when it comes to competition and innovation, I want to tie up a couple of loose ends.

Quadratic regression on log(y+1), programmed in Stan

In fitting the above multilevel hinge regression, I moved from the pre-programmed Stan code of stan_glmer() to a custom Stan program. Just to check that nothing funny is going on here, I’ll go back and program the multilevel quadratic regression directly in Stan. It’s easy enough to write the program; I just replace the hinge by a quadratic function and get rid of the priors, and, indeed, we get essentially the same result as when fitting using stan_glmer(). I won’t bother showing the new graph here. No surprise, it’s just good to check.

The other thing we can do with the Bayesian fit is see whether the peak of the curve falls within the range of the data. The curve b0 + b1*x + b2*x^2 has its peak at x = -b1/(2*b2) (just take the derivative, set to 0, and solve for x), so we can compute the posterior distribution of this value from our simulations. It turns out that only 3 of the 4000 simulated curves has a peak outside the range of the data, so fair enough that, according to the fitted quadratic model (which I don’t like), the inverse U pattern is occurring within those bounds.

Adjusting for the group-level mean of the predictor

In general when fitting a multilevel model, it’s a good idea to adjust for the group-level mean of the predictor–in this case, the average value of x within each industry. Otherwise you have to worry about correlations between x and the varying intercepts. In this case, adding this group-level predictor doesn’t change much. I won’t share the result here just because I’ve already done a lot of work to write this up and there are enough other concerns with the analysis, but, yeah, it’s a good idea to include this predictor too.

Summary

OK, so what have we learned?

• The graph from the original paper (reproduced at the top of the above post) did not show a good fit because it didn’t display the adjustments for industry. We can see the pattern a lot clearer using separate plots for each industry.

• I think it makes more sense all around to model these data on the log(y+1) scale rather than using Poisson regression or any of its variants.

• The patterns within and between industries aren’t so clear to me. I don’t get why furniture has so many patents, why the number of patents for machinery and computers dropped, why the number of patents for electric and gas services shot up, and so forth. I’m not saying these numbers are wrong, and I might have made some mistake in coding; I’m just saying I’m baffled.

• I think the hinge model is much more appropriate than the quadratic for the propose of seeing the extent to which the data support an inverted U pattern. It wasn’t hard at all to program, debug, and fit the hinge model, and in this case it does support the inverted U. So in that sense the published paper was correct in its statistical conclusion, even if I think they got kinda lucky in finding the pattern with their quadratic curves.

• I still don’t buy the claim in the paper that they “find strong evidence of an inverted U relationship” between “product market competition and innovation.” Again, my main problem here is their measure of innovation using average weighted patent counts, an issue that further bothers me given the odd data patterns seen in the graphs for some of the industries, also with the selection in the data (“Our sample includes all firms with names beginning “A” to “L” plus all large R&D firms. After removing firms involved in large mergers or acquisitions and those with missing data . . .”).

• Also the model predicts y from x in the same year, and we’d expect a lag. I didn’t bother addressing this because of my other concerns about the data.

I guess that later work followed up with more comprehensive data sources, but I remain concern that any inverse U pattern, even if supported by this particular dataset, could depend strongly on various artifacts of the measures they are using. There aren’t really a lot of data points at high values of x here, so this downward slope is defined by how these patents are being counted in just a couple of industries.

All this might sound like picky criticism, but it’s the authors of the paper (and the Nobel prize committee), not me, who are making these broad claims about competition and innovation, and concerns about measurement seem really important here.

That said, it’s cool to see that a careful statistical analysis does find the inverted U. It does seem like a real pattern in the data, so the only question is the relevance of these data to the larger economics question.

tl;dr

In response to one of the comments below, I wrote that I don’t at all trust the idea of using time variation of patents within an industry to measure time variation of innovation. I get that the authors were doing their best using available data; still, I don’t think their data and analysis provide evidence for their substantive conclusions.

In the immortal words of John Tukey, “The combination of some data and an aching desire for an answer does not ensure that a reasonable answer can be extracted from a given body of data.”

Looking at it that way, all my statistical analysis with the transformations and the quadratic curves and the hinge function was all a waste of time, as I’m just doing a fancy analysis of bad (or, at least, irrelevant) data. But . . . summarizing the statistical information still has value in itself. My analysis just took a few hours, a small fraction of the time the authors must have spent on preparing, analyzing, and interpreting their data. I think it’s important, when doing statistical analysis, to do the best we can do, in this case accounting for all these sources of variation and uncertainty.

Or, to put it another way, yes, it would have been fine to dismiss the published results entirely given the problems with the data. But some of the problems with the data became apparent only after I made those plots showing the time series for each industry. At that point, all the fitting may well have been a waste of time–but I only thought of making the plots because I was trying to understand the puzzling fit.

All the links connecting theory, measurement, data, analysis, and conclusions are important.

P.S. All these data and measurement problems just leap out at us, but there’s a whole world of people out there who just accept these conclusions–even some of the graphs from that 2005 paper–as truth. For example I came across this post by political journalist Matthew Yglesias that just straight up accepts the iffy empirical claims from that paper. It’s tricky–journalists are busy, and it’s natural to think that a much-cited paper written by two Nobel prize winners and published in a top journal has to be correct. I don’t really know what to say, except that this is one of the useful functions of social media, to allow us to push back against default narratives. Not that the default is necessarily wrong, just that it can be wrong, and it’s hard for journalists to escape the bubble and recognize this.

P.P.S. There was some concern about the arbitrariness of the log(y+1) transformation so I also fit the model to sqrt(y), which is a standard variance-stabilizing transformation for count data. The results looked essentially the same:

So the inverted U really seems to be there–but you have to assume the curve has the same shape for all industries. If you fit a separate curve for each industry, there’s no way you’d find the U, and you can see that in the scatterplots. The trouble is that the data are too sparse and variable to try to estimate a separate curve for each industry. Just look at electric and gas services, for example. Or passenger transit.

Data and code

Continue reading →

{kind=link}