Palko points to this post from Molly White, who writes:

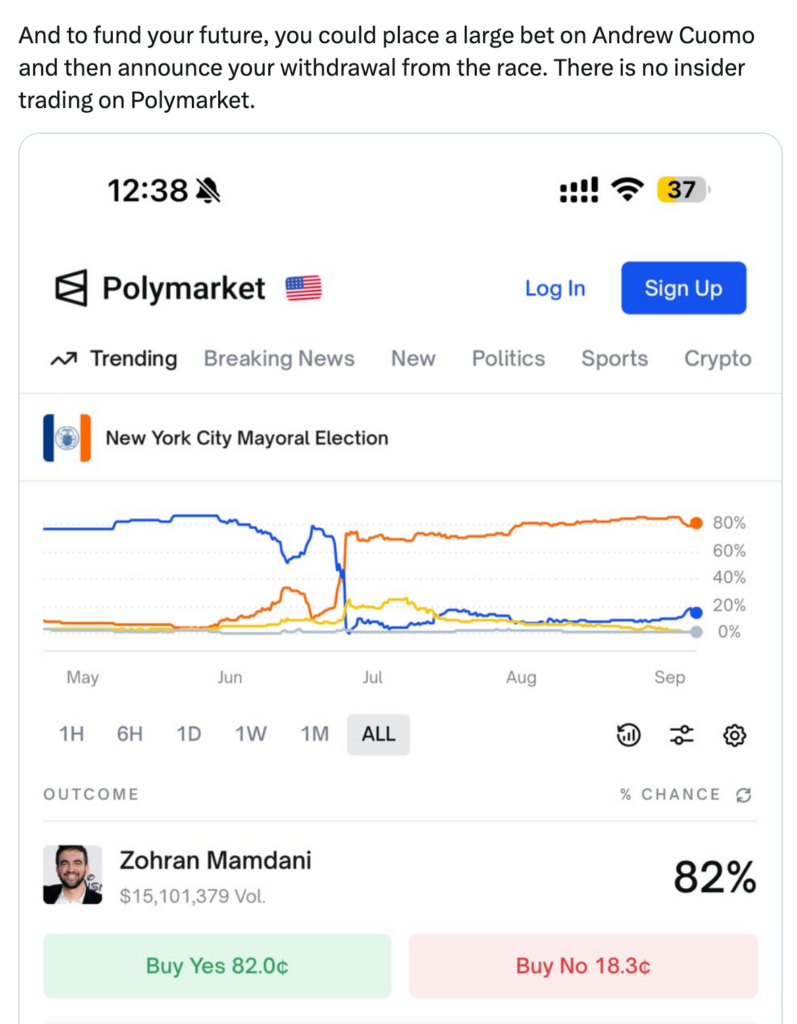

When billionaire Bill Ackman suggested on Twitter that Eric Adams could “place a large [Polymarket] bet on Andrew Cuomo and then announce [his] withdrawal” from the New York City mayoral race, he described something that feels profoundly illegal. A politician profiting from non-public knowledge of their own withdrawal from an election surely crosses some line — insider trading? Market manipulation? Election interference? Illegal gambling? Ackman ended his tweet: “There is no insider trading on Polymarket” — not because it doesn’t happen, but because it won’t be charged. He’s right: the Securities and Exchange Commission’s insider trading rules don’t apply here. But that leaves the question: what rules, if any, do?

As Ackman says, prediction markets fall outside the SEC’s jurisdiction,a living in a different regulatory world than stock markets where executives get prosecuted for trading on non-public earnings or tipping off friends about upcoming mergers. . . .

White continues:

Prediction markets — platforms where people trade contracts that pay out based on whether specific events happen — have enjoyed a surge in popularity over the last few years as they’ve dramatically expanded their operations in the United States. While they have existed for decades, they were long confined to strictly academic exercises — operating as small-scale non-profits that carefully constrained their operations to avoid running afoul of the CFTC. . . .

In 2020, the US-based Polymarket began allowing customers to use cryptocurrency to trade events contracts, though they made no effort to certify their contracts with the CFTC. In 2021, Kalshi emerged as the first fully regulated prediction market in the US, following a hard-won CFTC approval. . . . The CFTC cracked down on prediction markets in 2022. . . . when a district court ruled in Kalshi’s favor in 2024, the company swiftly reinstated the contested markets. The regulatory landscape shifted further after Trump took office. . . .

Finally:

Though prediction markets aren’t a new phenomenon, their growing accessibility to retail traders is. . . . The CFTC has yet to bring any enforcement actions pertaining to market manipulation on events contracts, and it’s not clear they have much appetite to begin doing so.

Other industries that deal with outcome-based bets, like sports wagering, have evolved robust integrity systems both to protect consumers and to preserve trust in the games themselves. . . . Today, sports betting platforms work to screen out athletes, referees, and sports program employees to ensure they’re not betting on games they could potentially influence, and employ monitoring programs to detect suspicious bets. . . .

While Kalshi imposes strict trading restrictions on its presidential election market — barring politicians, campaign staff, pollsters, election officials, and foreign nationals — many of its other markets lack any such prohibitions. This includes election-related markets identical to the type of bet Ackman suggested Adams could place on Polymarket about his own mayoral campaign withdrawal.

Polymarket, which does not yet serve US customers, does no such screening. The platform merely asks users to self-certify they aren’t US-based, with additional basic geofencing that users regularly circumvent. . . .

White summarizes:

Without much oversight, these markets are ripe for manipulation. The gambling-like nature of many markets, combined with limited addiction prevention programs, likely puts vulnerable users at risk. And election markets create concerning new financial incentives that could further corrupt democratic processes.

This does seem like a serious concern.

At one level, this is a problem that should cure itself, in that a few high-profile cases of manipulation should be enough to drive any serious bettors out of the market, so that it just becomes something more like a game of poker than anything else, and the total dollars in the market would not be enough for anyone to make much money by throwing an election, or a sporting event. On the other hand, lots of bad things could happen in sports and politics on the way to this eventual equilibrium. Also, in the absence of serious regulation, we should not underestimate the abilities of cheaters and scammers to come up with new clever means of corruption. So, yeah, I feel like we should be worried.

Another take

Along similar lines, here’s a related post, Prediction markets and the need for “dumb money” as well as “smart money” where I discuss similar ideas that were presented by people who are more politically conservative–they’re less concerned about market manipulation and more concerned that the prediction markets will fall apart on their own.

It’s interesting to juxtapose these two different, but related, lines of criticisms of prediction markets, with one set of criticisms coming from the left and the other coming from the right.

Difference from sports

The post linked just above discusses various differences between news-based prediction markets and sports betting.

Relevant to the NYC mayoral race discussion, one difference is that, in sports, throwing a game to win a bet is one of the main ways that corruption can enter the system. If there is no betting, it’s much harder to have any motivation to throw a game. In contrast, in politics there are lots of ways to benefit from dropping out, especially in today’s political environment where the national government is pretty openly dropping prosecutions of political allies or threatening political opponents. As we discussed in this game-theory-heavy post, there are lots of ways that Adams could corruptly benefit from strategically dropping out, and indeed these are methods that could be both easier and more lucrative than trying to manipulate betting markets. Indeed, if the government doesn’t want to offer Adams some position for which he is unqualified, Bill Ackman himself could just hire Adams for some no-show job in his organization at a salary of a million dollars a year, no?

So, given everything that’s been talked about in the mayoral election so far, it doesn’t seem that prediction markets represent much of a change to the moral, financial, and political calculations of corrupt maneuvering in a political race. It still seems disturbing, though, in the same way that it’s disturbing when politicians decide that various sleazy activities, which in the past they would have tried to hide, are now done in the open. And also disturbing in the potential pollution of the signal offered by prediction markets themselves.

This may also be the consequence of an unregulated market: Polymarket is not paying on bets that Venezuela would be invaded before January 31. Polymarket issued a statement that the capture of Maduro does not meet the definition of “invasion”:

https://www.theguardian.com/world/2026/jan/07/wager-platform-polymarket-will-not-pay-out-on-bets-on-us-invasion-of-venezuela

Also, the article states that, shortly before the capture of Maduro, a bettor placed a $30k bet that Venezuela would be invaded and won $400k.

So, to stress the point of Andrew’s post, this is an unregulated market with opaque rules.

The guardian article links here, which resolved to yes:

https://polymarket.com/event/maduro-out-in-2025/maduro-out-by-january-31-2026-318

Where do they link to a controversial invasion bet?

From the article:

“Last Friday an anonymous trader on Polymarket appeared to invest $30,000 (£22,343) on the market: Maduro out by 31 January 2026. After Maduro’s capture was announced on Saturday morning, the trader seemed to have made profits of $436,759.61.”

Thats the bet I linked, the bettor won because Maduro was deemed out.

Thinking about it more, we should also take into account that outlier bets are often hedges. Eg, my retirement account doesn’t allow shorting so I sometimes buy there and then later short in my other account if I think it may drop but don’t want to actually sell. Or vice versa, sell and then buy some cheap calls just in case.

Here’s the “invasion” bet that hasn’t resolved to Yes yet.

https://polymarket.com/event/will-the-us-invade-venezuela-in-2025?tid=1767825492561

And what if Cuomo does the same thing?

If this type of thing happened with any frequency, it would be priced in. Indeed, placing a bet large enough to be worthwhile will drive up the price, possibly buying the entire order book. I don’t see any problem with it, and insider trading/betting is already assumed to be rampant anyway.

Anon:

Interesting. Here’s a question. Suppose that, during the last week of the campaign, Cuomo had bet a couple million dollars on himself to lose, and then, once the bet was in, he had officially dropped out of the race–and publicly announced that he’d done so because he realized he was gonna lose so he decided to convert the “potential energy” of his position into the “kinetic energy” of some free money. So he would’ve made several hundred thousand dollars on the bets.

What would’ve happened? It would’ve been scandal, for sure, but could Cuomo have collected on the bet? According to wikipedia, “Polymarket blocked access to U.S. customers from 2022 to December 2, 2025, following a settlement with the Commodity Futures Trading Commission, which accused the company of running an unregistered derivatives-trading platform.” So maybe this option wasn’t really available?

I think polymarket wouldn’t pay out unless they had a proxy bet for them. But, I meant what if both candidates bet against themselves then drop out?

One argument against insider trading in the stock market is that if lots of people think they are at an informational disadvantage they won’t buy stocks and this will decrease the amount of capital available to companies to invest in productive activities. But if lots of people think they are at a similar disadvantage in sports or political betting so stop doing it then so what? A deep and liquid stock market has broader benefits to society which an expansion in recreational gambling does not.

Good points. Presumably there is a “Goldilocks” situation here for Polymarket? Part of the appeal of any type of trading is presumably the feeling that one’s predictions are good (and insider information is a scale rather than binary), so I imagine that Polymarket would like people to **think** that they can beat the market with some information, but they don’t want the extreme situation where the market becomes pointless.

Destroying a recreational gambling market is obviously *less bad* than destroying the stock market, but conversely, the likely impact of insider trading on the gambling market is a lot bigger. Buying stocks is not supposed to be a zero-sum fair bet — stocks, broadly speaking, go up — so you can have some insider trading without a disaster. In a pure gambling setup, fairness is much more load-bearing. If someone with inside knowledge is betting against you, you are going to lose money on the gambling market, but you’ll still probably make money on index funds (though perhaps not on day trading).

True, but I don’t see this as an argument for the government to regulate insider trading in gambling markets the way it does in financial markets. Using public resources to do so would essentially be a subsidy to the gambling industry.

Mark:

I don’t know. Consider the scenario described above. It seems a little disturbing, no?

Something interesting about Kalshi is that about 90% of the trading volume there is on sports. They are a sports gambling platform with a relatively small side-business running a prediction market, despite what their marketing would have you believe.

The people who are strong theoretical supporters of prediction markets see the benefit as producing good predictions. They can aggregate a wide variety of information, including non-public information.

From that perspective, insider trading isn’t necessarily bad; it makes the markets more informative by aggregating private insider knowledge. The danger is that this scares off enough dumb money that the markets become uninformative. But of course if the markets are uninformative that makes it easy to make money against them…

There’s some sweet spot here but it probably involves non-zero insider trading.

If dumb money is truly dumb, is it scared of insider trading?

Jay –

“from that perspective, insider trading isn’t necessarily bad…”

I don’t know about necessarily, but I think it’s just bad if people who have influence on government policy at heavily invested in creating a market where people bet on whether countries will be invaded, or even whether nuclear bombs will be dropped, etc.?