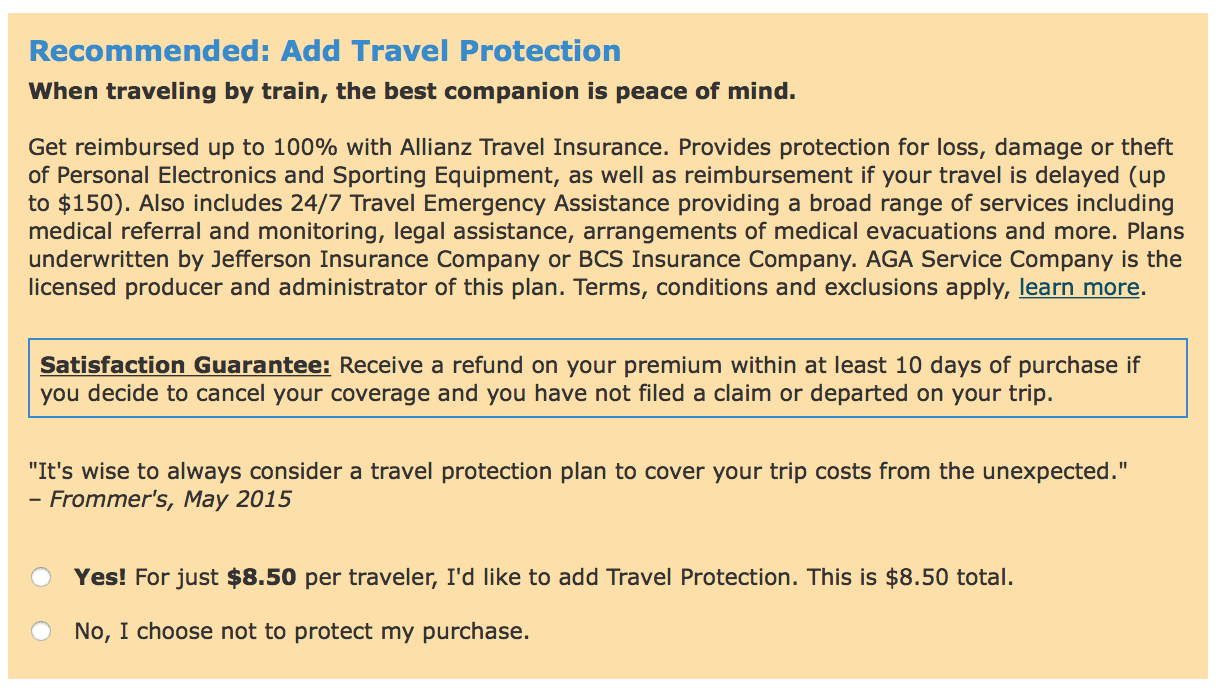

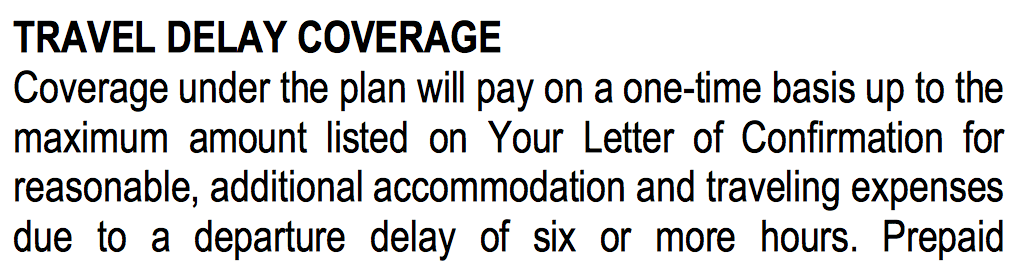

Hmmmm, coverage for travel delay, that might not be so bad. This is Amtrak, after all. Let’s click through to the fine print:

They’ll cover me for a departure delay of six or more hours, huh?

Nice try in your attempt to scam me out of $8.50. It didn’t work this time, but, hey, why not waste everyone’s time figuring out which little box to click? I’m sure you did some A/B testing and found there was a large enough pool of suckers to make it all worth it for you.

Assholes.

Once was waiting for the train at UC Davis to take me to the Martinez station down near the SF Bay. My train was delayed 2 hrs because a train from Colorado had to come through… 48 hours late.

Yeah, but they only get the reimbursement if the departure is more than 6 hours late.

Ahhh! I didn’t grok that bit. Sneaky!

Right, they’ll pull 100 feet out of the station and sit on a siding for 2 days.

Even if evil this seems run of the mill evil. Don’t they try this con every time I buy a flight ticket? “Trip Cancellation Coverage” or something they call it.

Rahul:

I can’t remember if Expedia does this too. But the Amtrak version seems particularly evil because (a) $8.50 is a lot compared to the price of a plane ticket, and (b) they’re covering us for something that will never happen.

And, what does “within at least 10 days” mean? “Within 10 days” means 10 or fewer days. “At least 10 days” means 10 or more days.

So, I guess the guarantee only applies if you choose to cancel the coverage on exactly the tenth day from the time of purchase. Naturally, if that happens to be a weekend or a holiday, you’re SOL.

I defense of Amtrak, I had a very pleasant trip from ME to MA last month. The ticket cost me $20 and trip was faster than it would have been in traffic going south on a summer Sunday afternoon.

(I know that has nothing to do with topic. I just want to show Amtrak a little love.)

Chris:

I actually love riding Amtrak. They’re still evil.

I’m surprised no one’s mentioned the Rabin-Gelman calibration theorem.

“We are all endowed with thousands of small risks in life, and because we are risk averse over each of these bets, profiteers will be tempted to sell us insurance policies on all of these small risks. How might potential money pumpers go about offering a collection of individual bets that a person will accept even though it bankrupts him? The cheapest and most direct way would be to offer a person all potential insurance policies collected together as one grand insurance policy sold at an exorbitant price. But this would not work against myopically loss-averse agents, because it is precisely for collections of bets presented together that myopically loss-averse agents act reasonably risk neutral. It is only the one-at-a-time, small-scale risks for which they are willing to pay tremendous insurance rates. Because a series of unattractive bets that is blatantly presented together is going to be rejected, Dutch bookies must be circumspect when setting out to exploit myopic loss-averters and would have to offer these unattractive bets one at a time. Information and transactions costs will prevent them from taking advantage of most of these small-scale trades, but for those small-scale insurance policies that can be sold without incurring large marketing expenses—such as when a customer is already buying a good or service—such policies will be sold. Hence, in an economy of myopic loss averters, we would see widespread sales of opportunistic, small-scale insurance sold at exorbitant prices that are inconsistent with expected utility theory, but also see many similar-sized risks left uninsured.

“Well, ***this is exactly what we see in the world.*** Expected utility theory predicts that people buy insurance that features large deductibles and very deep coverage (high maximum payouts). Instead, most insurance policies (like auto and health) are of precisely the opposite variety: low deductibles and low limits. Even greater perversions, such as collision-damage waivers on car rentals and extended warranties on household appliances, are precisely the kinds of policies people buy if they are myopically loss averse. Indeed, internal wiring protection of the type discussed by Cicchetti and Dubin (1994) is a perfect illustration for the sort of insurance we should expect to see sold to myopic loss-averters. All said, myopic loss averters are subject to many short Dutch chapters in their lives, but not to Dutch books.”

http://pubs.aeaweb.org/doi/pdfplus/10.1257/jep.15.1.219

Nice, but the paper is Rabin and Thaler, how did Gelman get on there? ;-)

Also… sigh, this pretty well explains the current problems with “Health insurance”.

Daniel:

I’ve never actually talked with Yitzhak about this stuff, but the basic idea is in section 5 of this paper from 1998. Considering I was doing this as a class demonstration in 2993 or so, I can only assume the idea was well known for many years before. I never wrote it up as a theorem because it seemed too obvious—or, to put it another way, it seemed too clear that risk aversion could not reasonably be explained in terms of a curving utility function for money. For decades I’ve been frustrated that this has been the standard story in economics. It seems like a triumph of ideology (not political ideology, but intellectual ideology) over logic.